![]()

Rails Over Rhetoric: Why the Lobito Corridor Is America’s Most Important Africa Bet — and Its Riskiest

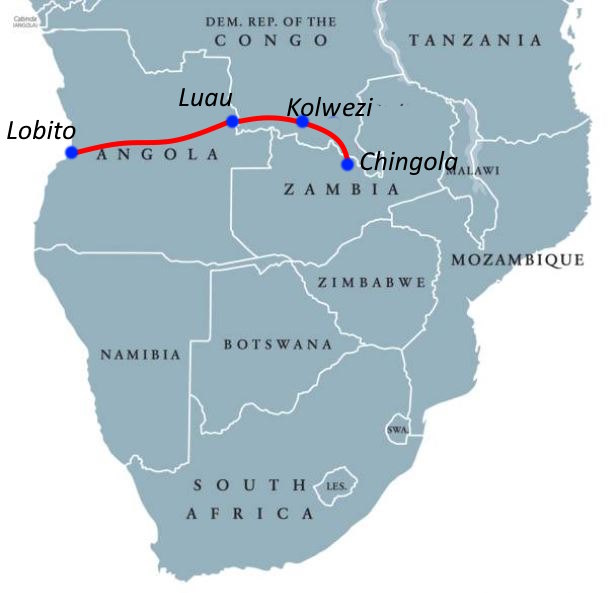

In February 2026, construction crews broke ground on the Lobito Corridor’s greenfield extension, a 1,744-kilometer rail-and-port concession connecting Angola’s Atlantic coast to the copper- and cobalt-rich heartland of the Democratic Republic of Congo and Zambia. It was a quiet moment by Washington’s standards: no prime-time coverage, no presidential address. Yet what is taking shape along that railway spine may prove to be the most consequential U.S. infrastructure commitment to Africa in a generation, and one of the clearest tests of whether American strategic engagement on the continent has finally moved beyond rhetoric into something durable.

The scale of investment reflects the stakes. Global commitments to the corridor now exceed $6 billion, anchored by over $4 billion in total U.S. investment including a $553 million loan from the U.S. International Development Finance Corporation covering the corridor’s 1,300-kilometer Angolan segment, alongside a $500 million African Development Bank pledge for broader corridor development and PGII commitments structured to generate at least $200 million more from the private sector. The project is led by the LAR Consortium under a 30-year concession, with Africa Finance Corporation serving as the greenfield extension developer, bypassing the slow-moving state funding models that have stalled African infrastructure for decades. The corridor is projected to slash transit times from the Copperbelt to Atlantic export terminals from 45 days to 15, and LAR has already procured 275 new container wagons from South Africa’s Galison Manufacturing to begin building the freight capacity that long-haul mineral logistics require. These are not aspirational figures; construction has started and the financing architecture is largely in place.

The Geopolitics of Track Gauge

The corridor’s strategic rationale is inseparable from the minerals it is designed to move. The DRC exported a record 3.1 million tonnes of copper in 2024, a 13 percent increase from 2023 that cemented its position as the world’s second-largest copper producer. Yet DRC copper exports fell 17.3 percent in the first nine months of 2025 due to operational and logistical constraints at key mines, demonstrating precisely the bottleneck the corridor is designed to break. Global copper demand reached approximately 26.9 million tonnes in 2025, and analysts project the market will tighten further in 2026, with a refined copper deficit of roughly 330,000 tonnes and LME prices forecast to average nearly $12,000 per tonne. S&P Global projects demand will reach 42 million tonnes by 2040, a 50 percent increase from current levels driven by electrification, electric vehicles, and AI infrastructure. These are not peripheral commodities. Copper and cobalt from the Copperbelt are foundational inputs for clean energy grids and defense electronics, and the United States currently sources almost none of them through supply chains it controls or can credibly influence.

China recognized this long before Washington did. Beijing spent decades building infrastructure and offtake agreements across the Copperbelt, and today Chinese state-owned and affiliated firms dominate DRC copper operations: CMOC alone produced over 650,000 tonnes from its DRC operations in 2024, accounting for a substantial share of the country’s record output. Whoever controls the logistics corridor to the coast controls a decisive chokepoint in the global clean energy supply chain, and for most of the past two decades, the infrastructure servicing that chokepoint was built to Chinese specifications. The Lobito Corridor, backed by PGII and the EU’s Global Gateway, represents Washington’s clearest attempt to build a competing logistics corridor rather than merely issue competing statements. That the corridor bypasses slow-moving state financing through a private concession model is itself a strategic choice, one designed to move at commercial speed rather than bureaucratic pace.

From Export Pipe to Two-Way Street

A logistics corridor is only as transformative as the economic ecosystem it enables, and on this dimension the Lobito Corridor faces its defining test. The project’s immediate value proposition is moving raw minerals westward to global markets. This is necessary but insufficient. Informal cross-border trade already accounts for 30 to 40 percent of total intra-regional trade in Southern Africa, and the corridor’s infrastructure upgrades are expected to facilitate significant additional volumes of agricultural products, processed goods, and manufactured items in both directions. Meeting that potential requires the corridor to function as a two-way economic artery, not a one-way extraction channel. A rail line optimized solely for raw mineral export replicates the colonial-era infrastructure logic that has historically captured value for distant markets rather than corridor communities. The corridor’s architects have committed to developing value-addition zones along the tracks where raw minerals are processed into intermediate products before export, but commitments require governance frameworks to become reality.

The Governance Gap

Three structural reforms are non-negotiable if the corridor’s economics are to match its ambitions. First, customs harmonization across Angola, the DRC, and Zambia is urgent. Modernization of the Dilolo-Sakania border link is underway, but multi-day border delays remain standard across the region, threatening to absorb much of the 30-day transit time gain on the rail line itself. The African Continental Free Trade Area provides the legal scaffolding for harmonized procedures; what is absent is the political will and operational capacity to implement them at speed. Second, structured local economic integration must be embedded from the outset rather than designed as an afterthought. USAID has allocated $4.5 million toward workforce development and agricultural industrialization along the corridor, a figure that is modest relative to the overall investment envelope and will need to scale materially if small and medium enterprises are to capture a meaningful share of the logistics, services, and processing opportunities the corridor creates. Third, the 30-year concession structure, while commercially sound, creates a long window in which opaque revenue flows can become entrenched. The U.S., EU, and African Development Bank must use their co-financier leverage to insist on open contracting standards, independent auditing, and enforceable community benefit agreements from the start of operations, not as conditions attached after problems emerge.

The Stakes Are Higher Than Trade

The Lobito Corridor is ultimately a test of whether the United States and its partners can offer Africa a structurally different model of engagement, one grounded in transparent investment, local value-addition, and long-term partnership rather than the fast-moving, low-conditionality approach that allowed China to embed itself so effectively across the continent. The numbers are significant: more than $6 billion committed, record Copperbelt mineral output, a 30-day transit reduction that could transform regional trade competitiveness, and a financing architecture built around private capital rather than sovereign debt dependency. But infrastructure is the skeleton; governance is the soul. Without customs reform, genuine local inclusion, and anti-corruption commitments enforced across the full 30-year concession, the corridor risks becoming the most expensive extraction upgrade in African infrastructure history. The rails are going down. Ensuring the trains carry Africa’s future, not just its resources, is the work that now defines whether this investment delivers on its promise.